In this page we will explain the topics for the chapter 8 of Comparing quantities Class 8 Maths.We touched upon the concept of discount,Profit ,loss,Simple and compound interest. Here we have given good quality Comparing Quantities Class 8 Notes along with video to explain various things so that students can benefits from it and learn maths in a fun and easy manner, Hope you like them and do not forget to like , social share

and comment at the end of the page.

Quick Revision of Unitary Method,Ratio and Percentage

Unitary Method

Unitary method is on the most useful method to solve ratio, proportion and percentage problems. In this we first find value of one unit and then find the value of required number of units.

So in Short Unitary method comprises two following steps:

Step 1 = Find the value of one unit. Step 2 = Then find the value of required number of units.

Example

If 9 kg Mangoes costs Rs.450, then how much 8 Kg Mangoes will costs? Solution

By unitary Method

9 kg Mangoes = Rs.450

1 kg Mangoes = Rs.450/ 9 ( unit price)

8 kg Mangoes = Rs. (450/ 9)*8 = Rs.400

Percentages

Percentages are ways to compare quantities. They are numerators of fractions with denominator 100 or it basically means per 100 value

Per cent is derived from Latin word ‘per centum’ meaning ‘per hundred’

It is denoted by % symbol

1% means 1/100= .01

We can use either unitary method or we need to convert the fraction to an equivalent fraction with denominator 100

Example

4 out of 10 shirts are Red. What % of shirts are red? Solution

By Unitary method

Out of 10 shirt ,the number of red shirts are 4

Hence, out of 100, the number of red shirts are

= (4/10)×100 = 40

So 40%

By Fraction method

The ratio is 4/10

= (4/10) × (10/10)

=40/100

So 40%

Finding Discounts

Discount is a reduction given on the Marked Price (MP) of the article.

This is generally given to attract customers to buy goods or to promote sales of the goods. You can find

the discount by subtracting its sale price from its marked price.

So, Discount = Marked price – Sale price

Example

In Big Bazar an item of Rs 800 is sold for Rs 640. What is the discount and discount %? Solution:

Discount = Marked Price – Sale Price

= Rs 800 – Rs 640

= Rs 160

Since discount is on marked price, we will have to use marked price as the base.

By unitary method

On marked price of Rs 800, the discount is Rs 160

On MP of Rs 100, how much will the discount be?

Discount = (160/800)X100=20%

By Fraction method

160/800 = (4/20) X (5/5)

= 20/100 =20%

Profit and Loss

Cost Price : It is the actual price of the item

Overhead charges/expenses :These additional expenses are made while buying or before selling it. These expenses have to be included in the cost price

So Cost Price: Actual CP + overhead charges

Selling Price: It is price at which the item is sold to the customer

If S.P > C.P, We make some money from selling the item. This is called Profit

Profit = SP – CP

Profit % = (P/CP) X 100

If S.P < C.P, We loose some money from selling the item. This is called Loss

Loss = C.P – S.P

Loss % =( L/C.P) X 100

Example

A shopkeeper purchased 200 Maggi for Rs 10 each. He sold them at Rs 12 each. Find the ain or loss %. Solution:

Cost price of 200 Maggi = RS 200 × 10 = ` 2000

The SP of 200 Maggi = Rs 200 × 12 = Rs 2400

He obviously made a profit (as SP > CP).

Profit = Rs 2400 – Rs 2000 = Rs 400

On Rs 2000, the profit is Rs 400

On Rs 100, the profit would be

=(400/2000)X100= 20%

Watch this tutorial for more explanation About Profit and Loss

Sales Tax and VAT

Sales Tax(ST)

This is the amount charged by the government on the sale of an item.

It is collected by the shopkeeper from the customer and given to the government. This is, therefore, always on the selling price of an item and is added to the value of the bill. Value added tax(VAT)

This is the again the amount charged by the government on the sale of an item. It is collected by the shopkeeper from the customer and given to the government. This is, therefore, always on the selling price of an item and is added to the value of the bill.

Earlier You must have seen Sales tax on the bill, now a days , you will mostly see Value Added Tax Calculation

If the tax is x%, then Total price after including tax would be

Final Price= Cost of item + (x/cost of item) X100

Watch this tutorial for more explanation About Sales Tax and VAT including example

Simple Interest and Compound Interest

Interest

Interest is the extra money paid by institutions like banks or post offices on money deposited (kept) with them. Interest is also paid by people when they borrow money

Simple Interest

Principal (P): The original sum of money loaned/deposited. Also known as capital.

Time (T): The duration for which the money is borrowed/deposited.

Rate of Interest (R): The percent of interest that you pay for money borrowed, or earn for money deposited

Simple interest is calculated as

$\text {Simple Interest} = \frac {P \times R \times T}{100}$ Total amount at the end of time period A= P + SI

Compound Interest

Principal (P): The original sum of money loaned/deposited.

Time (n): The duration for which the money is borrowed/deposited.

Rate of Interest (R): The percent of interest that you pay for money borrowed, or earn for money deposited

Compound interest is the interest calculated on the previous year’s amount (A = P + I).

So Ist Year

$A= P + \frac {P \times R}{100} = P (1 + \frac {R}{100})$

IInd year

$A= = P (1 + \frac {R}{100}) + P (1 + \frac {R}{100}) \frac {R}{100} = P(1+ \frac {R}{100})^2$

So N year will be given by

$A = P(1+ \frac {R}{100})^n$

The above formula is the interest compounded annually

Compound Interest Formula if the interest is compound half yearly

$A = P(1+ \frac {R}{200})^{2n}$

Here R/2 is the half yearly rate

2n is the number of half year

Similarly, for interest compounded quarterly

$A = P(1+ \frac {R}{400})^{4n}$

Watch this tutorial for more explanation About Simple interest and Compound interest

Example

(a) Find Compound interest for Rs 12600 for 2 years at 10% per annum compounded annually.

(b) Find the interest if it is not compound annually

(c) Compare them Solution:

(a)

$A = P(1+ \frac {R}{100})^n$

where Principal (P) = Rs 12600, Rate (R) = 10,

Number of years (n) = 2

$A = 12600(1+ \frac {10}{100})^2$

=15246

CI = A – P = Rs 15246 – Rs 12600 =Rs 2646

b)

If it is not compounded annually ie. Simple interest

$\text {Simple Interest} = \frac {P \times R \times T}{100}$

$\text {Simple Interest} = \frac {12600 \times 10 \times 2}{100}$

SI= Rs2520

c) It is clear that

CI > SI

Frequently asked Questions on CBSE Class 8 Maths Chapter 7: Comparing quantities

What are comparing quantities?

Comparing quantities means mathematical relationship between two quantities that reflect their height,weight, price etc. examples ratios, percentage,discount, interest, VAT

What is SP and CP?

SP stands for Selling price and CP stands for Cost price.SP is price at which the item is sold and CP is the actual price of the item

What is Gain Formula and Loss Formula?

Gain Formula is Gain= Selling Price - Cost Price or Gain = Revenue - expenses

Loss Formula is Loss=Cost Price - Selling Price

What is a Unit rate?

It is a value of 1 unit. Now that can be use to find the price of many items. Example Price of 12 pens is 120,then price of 1 unit is Rs 10. So that is the Unit rate

Loss Formula is Loss=Cost Price - Selling Price

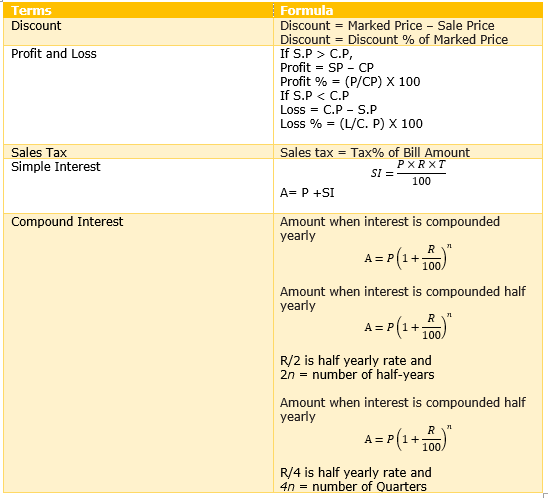

Summary of Formula Of comparing Quantities

Here is the Summary of Formula Of comparing Quantities Class 8 Notes